7 Things You Should Know HOA reserve funds

1. Laws regarding Reserve Funding Levels, Reserve Studies, and Reserve Contributions differ by state.

Reserve Study Laws and Reserve Funding Legislation vary by state. In the absence of specific legislation regarding Reserve Funding, associations should refer to their governing documents (Covenants Conditions, and Restrictions) with the help of a qualified attorney specializing in HOAs.

The following resources provide additional information regarding basic fiduciary duties of board members:

Council of Non-Profits “Board Roles and Responsibilities”

CAI Best Practices “Reserve Studies/Management”

Arizona Seller Disclosure Laws

2. Understanding the “Fully Funded Balance” is one of the most important factors to understanding a Reserve Study

This term is confusing to most homeowners and board members. Trying to explain this by providing a detailed mathematical formula will complicate things even worse!

In simple terms, the Fully Funded Balance represents the total accumulated depreciation for all Reserve Components. This still sounds complicated, so let’s use an example to explain:

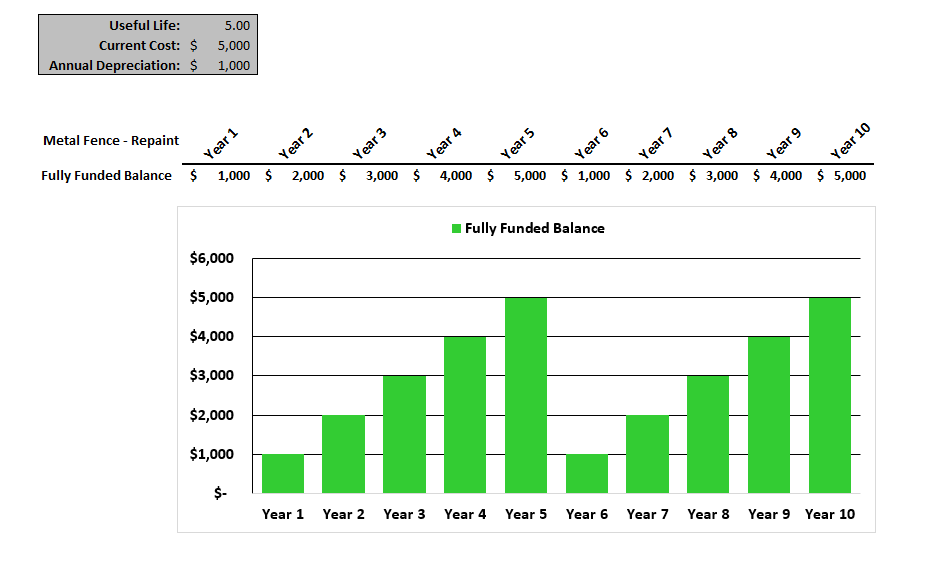

Association XYZ is responsible for repainting a Metal Fence. This Fence is repainted every 5 years at a cost of $5,000. The Fully Funded Balance for this View Fence is equal to the annual deterioration rate multiplied by the component age.

So, 1 year after installation, the FFB for this Fence would be $1,000 [($5,000/5-years) X 1 = $1,000]. The bar chart below illustrates the movement of the Fully Funded Balance for this Fence over time:

This basic formula is applied (with the effects of inflation) to all of the Reserve components at your association and the total is your FFB. Understanding the Fully Funded Balance is a crucial first step in understanding your Reserve Study.

3. Under-funding Reserves is never a good idea

Underfunded reserve levels always result in one of two outcomes; Emergency Funding in the form of Loans and Special Assessments or Deferred Maintenance resulting in lower property values and more costly repairs. The exact timing of future reserve expenses is unknown; however, the need for future repair and replacement of reserve components is a certainty. Failing to plan for the future with proper Reserve Contributions violates board members’ fiduciary duty and in some states is against the law.

Accounting tip of the day: Did you know? If you do not have a designated Reserve Fund Account, the IRS can view these funds as taxable income to the Association. Be sure to consult with your tax adviser regarding the separation of Operating and Reserve accounts.

4. A professionally prepared Reserve Study is an essential financial and strategic planning tool for board members

A responsible board member will contract with a qualified Reserve Professional to perform a Reserve Study to answer three basic questions:

- What physical assets does the Association own that will require future Association Funds?

- How much should we have in the Reserve Fund?

- How much should we save per month or per year in order to avoid underfunding Reserves?

5. Special Assessments and Loans are always more costly than proper Reserve Contributions

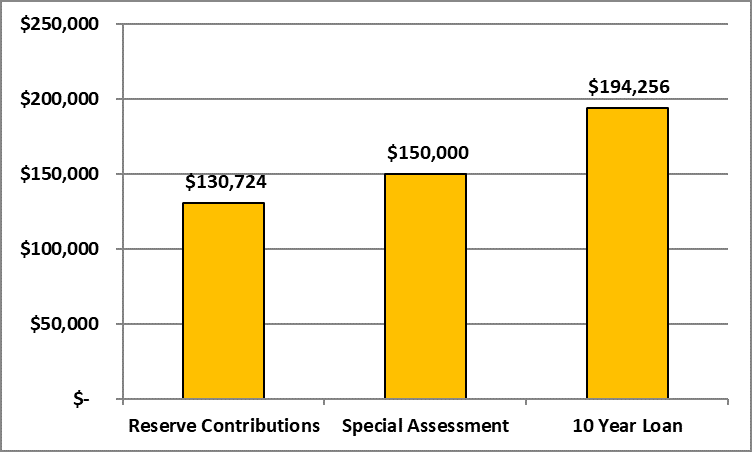

Because Proper Reserve Contributions often result in the need to raise annual assessments, board members will elect to “Save money” by cutting Reserve Contributions from the annual budget. This thinking is simply not true. Let’s compare the total cost to replace a Metal Fence in 20 Years at $150,000 with (3) Options: 1. Regular Reserve Contributions, 2. Special Assessment 3. 10-Year Loan at 5%.

Regular Reserve Contributions benefit from the compound effects of interest earnings so the required funding is actually less than the cost to replace the fence of $150,000. In addition to the cost savings of making Regular Reserve Contributions as illustrated above, another reason for adequate Reserve Contributions is to protect against potential liability resulting from years of under-funded reserves.

Board members who keep assessments low by ignoring the annual deterioration and funding requirements are not performing their “Fiduciary” duty. This scenario leaves future homeowners “holding the bag” and forced to raise emergency capital to replace the deteriorated fence. To avoid the above situation, monthly assessments should accurately reflect the cost of maintaining association-owned assets now and in the future. This is best done with the help of a professionally prepared Reserve Study.

6. Reserve Studies protect and preserve property values

A Reserve Study is a tool to be used by board members to assist in the proper management and guidance of the association’s present and future. When a professional Reserve Study prepared in accordance with CAI and APRA standards is followed, board members will fulfill their “Fiduciary” duty and avoid potential liability claims, homeowners will save money by avoiding Special Assessments and Loans, and funds will be available to maintain community assets translating into value for homeowners.

7. All Reserve Studies are not equal

Despite the similar goal of “Prepare now for the future”, Reserve Studies differ in methodologies and calculations. For example, A Reserve Provider using the “Modified Cash-Flow” approach will produce a report yielding different results than a reserve provider using the “Component Method” approach. When looking to hire a Reserve Specialist, be sure to understand the differences between these methodologies.

GET IN TOUCH